The maximum allowable offer (MAO) is the highest price a real estate investor should pay for a property while still protecting a target profit margin. Getting this number right separates profitable deals from costly mistakes. The standard formula used to determine maximum allowable offer is MAO = (ARV × 70%) minus estimated repair costs, where ARV stands for after repair value. This article breaks down that formula, expands it for rental property investors, and shows you how to adjust it for real market conditions.

What is the formula to determine your maximum allowable offer?

The core MAO formula is straightforward: MAO = (ARV × 0.70) minus rehab costs. The 70% rule is designed to cover acquisition costs, holding costs, selling costs, and a profit margin all within that 30% buffer. For example, if a property has an ARV of $200,000 and needs $30,000 in repairs, your MAO is ($200,000 × 0.70) minus $30,000, which equals $110,000.

That simple formula works well as a quick filter. For rental property investors who hold long term, a more detailed calculation gives you a better ceiling:

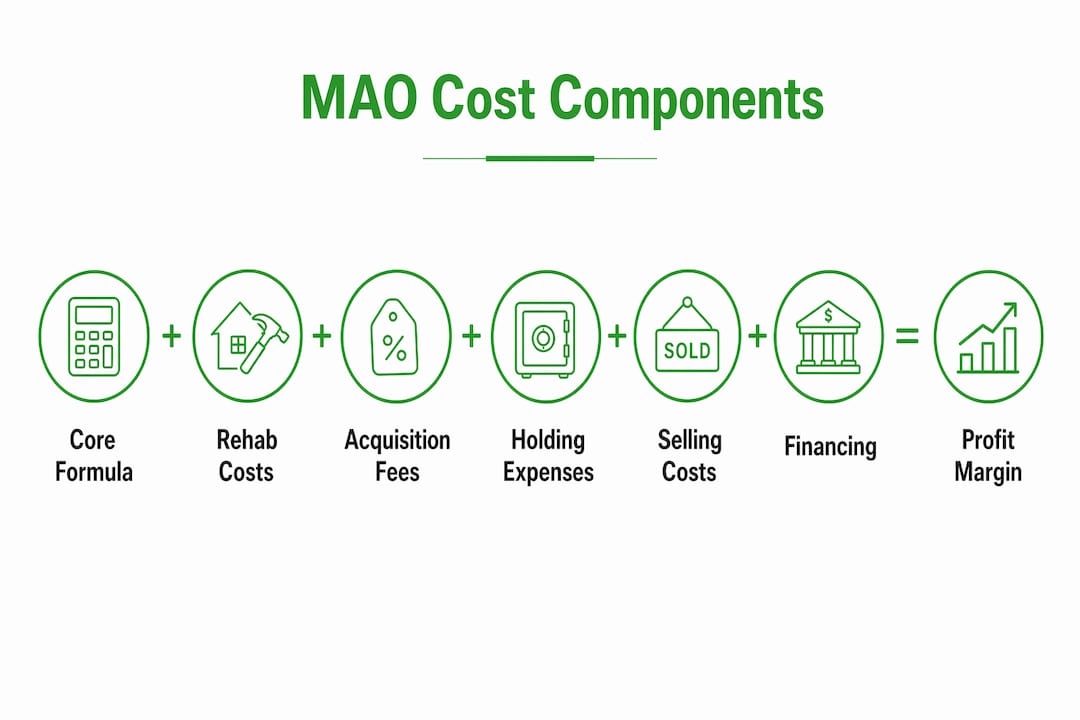

MAO = ARV − Rehab Costs − Contingency − Acquisition Costs − Holding Costs − Selling Costs − Financing Costs − Desired Profit

Here is how that plays out with real numbers:

| Input | Amount |

|---|---|

| After repair value (ARV) | $200,000 |

| Rehab costs | $30,000 |

| Rehab contingency (12%) | $3,600 |

| Acquisition costs (3.5%) | $7,000 |

| Holding costs (5%) | $10,000 |

| Selling costs (7.5%) | $15,000 |

| Desired profit (15%) | $30,000 |

| Maximum allowable offer | $104,400 |

Notice the detailed formula produces a lower number than the simple 70% rule. That gap matters. The simple rule often underestimates financing and holding costs, which means investors who rely on it alone can end up with thinner margins than expected.

One critical point: MAO is a ceiling, not a starting bid. Every dollar you offer above your calculated MAO comes directly out of your profit. Treat it as a hard limit, not a negotiating anchor.

- Calculate ARV using recent comparable sales within one mile and six months.

- Get a contractor estimate for rehab, then add your contingency buffer.

- Add up all cost categories using realistic percentages, not best-case assumptions.

- Subtract everything from ARV to get your true maximum bid.

- Never offer above that number, regardless of competitive pressure.

What cost components belong in your MAO calculation?

Every cost category that reduces your net return must appear in your MAO formula. Investors who skip categories do not save money. They just discover the missing costs later, after the deal closes.

Acquisition costs cover title insurance, escrow fees, transfer taxes, and lender fees. These typically run 3%–4% of ARV. Holding costs include property taxes, insurance, utilities, and loan interest during the renovation period. Holding costs average 4%–6% of ARV depending on your market and timeline. Selling costs include agent commissions, staging, and closing credits, which typically land at 7%–8% of ARV.

Rehab budgets deserve special attention. Contractor estimates are almost always optimistic. Experienced investors add a 10%–15% contingency to every rehab estimate to account for hidden issues. Older properties frequently reveal knob-and-tube wiring, mold, or foundation problems once walls open up. Those surprises can add 15%–20% to your original scope.

Financing costs are the most commonly ignored line item. Hard money loans carry origination fees of 1%–3% plus monthly interest rates that compound during your hold period. A six-month renovation on a $150,000 loan at 12% annual interest adds $9,000 in interest alone, before origination fees. Hard money costs must be integrated into your full formula, not treated as an afterthought.

- Acquisition costs: 3%–4% of ARV

- Holding costs: 4%–6% of ARV

- Selling costs: 7%–8% of ARV

- Rehab contingency: 10%–15% of contractor estimate

- Financing costs: varies by lender, typically 1%–3% origination plus monthly interest

- Desired profit: 15%–20% of ARV for standard deals

Pro Tip: Build your cost estimates from the worst-case scenario, not the average. If your deal still works at worst-case numbers, it will almost certainly work in practice.

How do you adjust your MAO based on market conditions?

The 70% rule is a starting point, not a fixed law. Market conditions, property type, and your investment strategy all require you to shift the multiplier up or down. The 70% multiplier should drop to 68% or lower when days on market are rising, competition is thin, or the property needs extensive work.

Rehab scope is one of the clearest signals for adjustment. A quick cosmetic flip with new paint, flooring, and fixtures can support a multiplier of 72%–75% because the hold time is short and cost risk is low. An extensive gut renovation with structural work, new plumbing, and electrical upgrades requires a multiplier of 65%–70% to account for the longer hold and higher cost uncertainty. Rehab scope directly drives the multiplier you should use.

Interest rate environments also shift your ceiling. When borrowing costs rise, your monthly carrying costs increase, which shrinks your MAO even if the ARV stays the same. A deal that worked at 7% interest may not work at 10% without renegotiating the purchase price.

- Hot seller's market: You may push toward 72%–75% if comps are strong and your rehab timeline is short.

- Balanced market: Stick to the standard 70% rule with full cost accounting.

- Buyer's market: Drop to 65%–68% to capture the additional negotiating room and risk buffer.

- Auction or limited-access property: Use 65% or lower, since you cannot fully inspect the property before bidding.

For auction situations, conservative multipliers around 65% protect you from unknown property conditions. You cannot walk through the property, pull permits, or get a full inspection before the hammer falls. That uncertainty has a real dollar cost, and your maximum bid must reflect it.

Pro Tip: Set your auction maximum bid before the event starts and write it down. Once bidding begins, emotion takes over. A written number keeps you honest.

Target profit margins typically range from 15%–20% of ARV for standard fix-and-flip or rental acquisition deals. Pushing above 25% makes your offers uncompetitive in most markets. Dropping below 15% may not justify the time, capital, and risk involved.

What tools and methods help you verify your maximum allowable bid?

Accurate ARV is the single most important input in any MAO calculation. A 5% error in ARV on a $200,000 property equals a $10,000 swing in your offer ceiling. Pull comparable sales from the MLS, county records, or a licensed agent within one mile and the past six months. Weight comps by similarity: same bedroom count, similar square footage, and comparable condition after renovation.

Rehab estimates require a licensed contractor walkthrough, not a visual guess. Get at least two estimates for any project over $20,000. Use the higher estimate as your baseline, then add your contingency on top of that. This approach builds in two layers of protection against cost overruns.

| Verification method | What it checks | Reliability level |

|---|---|---|

| MLS comparable sales | ARV accuracy | High |

| Licensed contractor estimate | Rehab cost baseline | Medium to high |

| County permit records | Hidden prior work or violations | High |

| Spreadsheet cost tracker | Full cost category totals | High when inputs are accurate |

| MAO calculator tool | Formula output and margin check | High when inputs are accurate |

Spreadsheet templates work well for tracking all cost categories in one place. They let you run multiple scenarios quickly by changing one variable at a time. Deal-zilla's Deal Analyzer tool takes this further by letting you input rehab costs, holding periods, and financing terms to generate a verified MAO in real time.

Pro Tip: Run your MAO calculation twice: once with your best estimates, and once with costs 15% higher across the board. If the deal breaks at the higher number, it is too thin to pursue.

What mistakes cause investors to miscalculate their maximum offer?

Emotional bidding is the most expensive mistake in real estate investing. Math-based discipline is the only reliable defense against overpaying, especially in competitive markets where fear of missing out pushes buyers above their calculated ceiling. The deal you walk away from is often the one that saves your portfolio.

Underestimating rehab costs is the second most common error. Investors who rely on visual walkthroughs without contractor input routinely miss plumbing, electrical, and structural issues. These hidden problems are not rare. They are the norm in properties over 30 years old.

- Skipping holding costs: A six-month renovation adds months of taxes, insurance, and loan interest that many investors forget to include.

- Using optimistic ARV: Pulling comps from a different neighborhood or a different market cycle inflates your ceiling and shrinks your actual margin.

- Ignoring financing costs: Hard money origination fees and monthly interest can reduce your MAO by $10,000 or more on a mid-size deal.

- Treating MAO as a starting point: Offering above your calculated ceiling because you "really want the deal" is how investors lose money on paper-perfect properties.

"The discipline to walk away from a deal that exceeds your MAO is what separates investors who build wealth from those who stay busy without profit."

Troubleshooting a deal that keeps falling apart at the offer stage usually points to one of two problems: your ARV is too high, or your cost estimates are too low. Pull fresh comps, get a new contractor estimate, and recalculate from scratch. Do not adjust the formula to make the deal work. Adjust your inputs to reflect reality.

Key Takeaways

Accurately calculating your maximum allowable offer requires realistic ARV, full cost accounting across all categories, and the discipline to treat the result as a hard ceiling, not a negotiating floor.

| Point | Details |

|---|---|

| Core MAO formula | MAO = (ARV × 70%) minus rehab costs; use the detailed formula for rental deals. |

| MAO is a ceiling | Never offer above your calculated MAO. Every extra dollar reduces your profit directly. |

| Include all cost categories | Acquisition, holding, selling, financing, and contingency must all appear in your calculation. |

| Adjust the multiplier | Drop below 70% for gut renovations, rising markets, or auction properties with limited access. |

| Verify with two scenarios | Run your MAO at normal estimates and at costs 15% higher to test deal strength. |

Why I stopped trusting the 70% rule on its own

The 70% rule is a useful filter for screening deals fast. After working through dozens of rental acquisitions, I stopped relying on it as a final answer. The rule was built for fix-and-flip timelines, not for landlords who hold properties for years. When you factor in longer holding periods, property management setup costs, and the financing reality of today's interest rates, the simple formula leaves too much room for error.

The most valuable shift I made was treating MAO as a living calculation, not a one-time number. Market conditions change between the time you run your first analysis and the day you close. I now recalculate MAO the week before any offer goes in, using fresh comps and updated contractor input. That habit has saved me from two deals that looked good at first glance but fell apart under current numbers.

For rental property investors specifically, the profit target calculation also needs to reflect cash flow, not just a one-time flip margin. A property that barely clears your MAO on a flip basis may still be a strong rental if the rent-to-value ratio supports long-term returns. Deal-zilla's BRRRR calculator handles this dual analysis well, letting you evaluate both the acquisition ceiling and the long-term cash flow in one place.

The investors I have seen struggle most are the ones who calculate MAO once, fall in love with a property, and then find reasons to justify going over their number. The formula is not the enemy of a good deal. It is the thing that keeps good deals from turning into expensive lessons.

— ARX

Deal-zilla makes calculating your maximum offer faster and more accurate

Running a full MAO calculation by hand takes time, and one missed cost category can throw off your entire offer strategy. Deal-zilla's platform gives real estate investors a purpose-built set of tools to calculate maximum offer prices with confidence.

The Deal Analyzer at Deal-zilla lets you input ARV, rehab costs, holding periods, financing terms, and desired profit in one place. It calculates your MAO instantly and flags deals where your margin is too thin. Whether you are evaluating a fix-and-flip, a BRRRR acquisition, or a Section 8 rental, Deal-zilla's tools are built for the numbers that actually matter to investors protecting their returns.

FAQ

What is the maximum allowable offer formula?

MAO = (ARV × 70%) minus estimated rehab costs. For more accuracy, subtract all cost categories including holding, selling, financing, and desired profit from ARV.

How do I calculate maximum offer for a rental property?

Use the detailed formula: ARV minus rehab, contingency, acquisition costs, holding costs, selling costs, financing costs, and your target profit. This gives a more accurate ceiling than the simple 70% rule for long-term holds.

What is a good profit target when setting my maximum allowable bid?

Target profit margins of 15%–20% of ARV are standard for most deals. Margins above 25% reduce offer competitiveness, while margins below 15% may not justify the investment risk.

Should I use a different multiplier for auction properties?

Yes. Use a multiplier of 65% or lower for auction properties where you cannot fully inspect before bidding. The unknown condition risk must be priced into your maximum bid.

What is the most common mistake in MAO calculations?

Underestimating rehab costs and skipping financing costs are the two most frequent errors. Add a 10%–15% contingency to every contractor estimate and always include hard money origination fees and monthly interest in your full calculation.