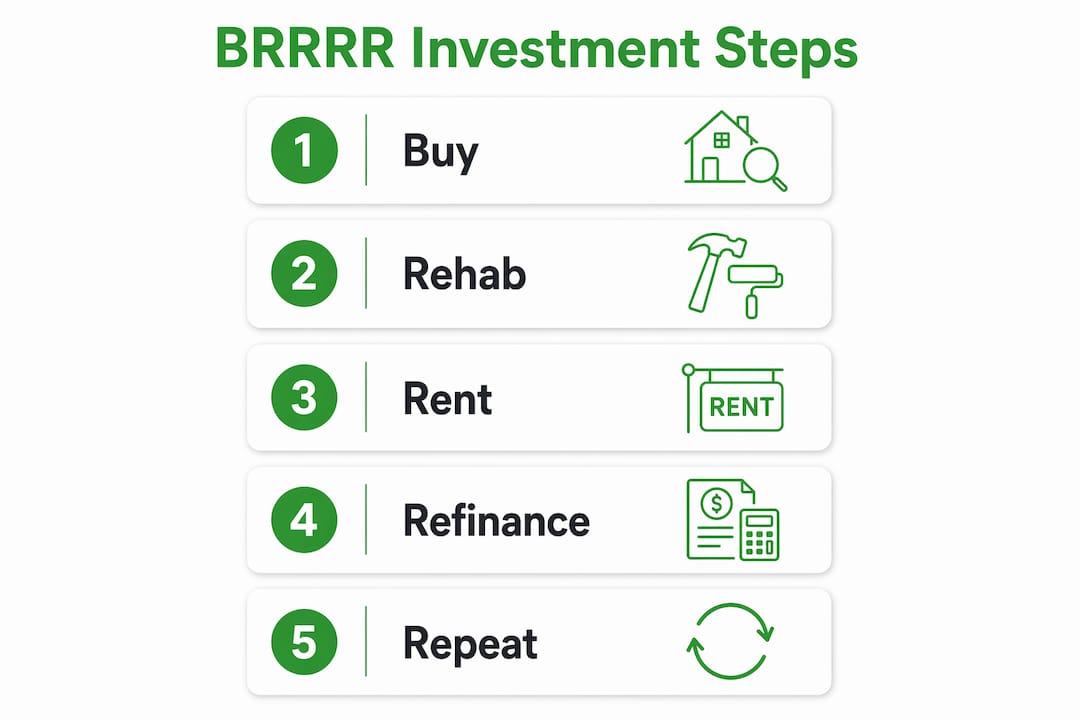

The BRRRR method is a real estate investment strategy defined by five steps: Buy, Rehab, Rent, Refinance, Repeat. Understanding why BRRR works for investors comes down to one core mechanic: you recycle the same capital pool across multiple properties instead of locking it up in a single deal. Traditional buy-and-hold investing ties up $50,000–$80,000 per property permanently. BRRRR breaks that constraint. The 70% rule and a target cash-out refinance LTV of 75% form the financial backbone that makes each cycle sustainable.

Why does the BRRRR strategy work for investors?

BRRRR works because it separates the act of acquiring an asset from the act of funding it permanently. You buy a distressed property below market value, force appreciation through renovation, place a tenant, and then pull most or all of your invested cash back out through a refinance. That recovered capital goes into the next deal.

The purchase formula is straightforward: (ARV × 0.70) minus repair costs equals your maximum offer price. ARV stands for After Repair Value, the estimated market value of the property after all renovations are complete. Buying at or below this number creates enough equity cushion to survive the refinance at 75% LTV and still walk away with cash in hand.

Traditional buy-and-hold investors must save a full down payment for every new property. A BRRRR investor can acquire multiple properties using the same initial capital pool over a five-year period. That compounding effect is the core reason the method builds portfolios faster than any standard rental acquisition approach.

How capital recycling accelerates portfolio growth

The table below shows the structural difference between traditional and BRRRR acquisition:

| Factor | Traditional buy-and-hold | BRRRR method |

|---|---|---|

| Capital per deal | Locked permanently | Recovered via refinance |

| Properties in 5 years | 1–2 (capital constrained) | 3–5 (same starting capital) |

| Equity creation | Market appreciation only | Forced appreciation plus market |

| Refinance trigger | Optional | Core to the strategy |

| Qualification method | Personal DTI | Often DSCR (property income) |

Key advantages of the BRRRR cycle over standard rental acquisition:

- Capital efficiency. One pool of money funds multiple deals sequentially.

- Forced appreciation. Renovations create equity before the market does anything.

- Cash flow from day one. A stabilized tenant in place before refinance proves income to lenders.

- Portfolio velocity. Faster acquisition means more doors, more rent, more long-term wealth.

Why is forced appreciation critical for BRRRR success?

Forced appreciation is the deliberate increase in property value through targeted renovations, and it is the engine that makes the refinance step possible. Without it, you are simply buying a distressed property and hoping the market bails you out.

The renovations that move appraisal values most are functional upgrades: adding a bathroom, updating a kitchen to a livable standard, replacing a roof, or upgrading HVAC systems. Over-renovating with luxury finishes does not yield proportional appraisal returns. A granite countertop in a B-class neighborhood does not add $10,000 to the appraised value. Spend where appraisers and tenants both respond.

Rehab budgeting accuracy is equally critical. Hidden structural problems, including foundation issues, outdated plumbing, or knob-and-tube wiring, appear only after demolition begins. Experienced BRRRR investors always add a 10–20% contingency to their rehab budgets to absorb these surprises without blowing the deal math.

Pro Tip: Walk every property with a licensed general contractor before making an offer. A $500 inspection fee can prevent a $15,000 budget overrun that kills your refinance equity.

Rehab quality also affects tenant quality and rental income. A well-finished property in a stable neighborhood attracts tenants who stay longer and pay on time. That rental stability directly supports your refinance approval, because lenders want to see consistent income history before they release cash.

What lender requirements should BRRRR investors know?

Lenders do not refinance a freshly renovated property the day you finish work. Most require a seasoning period of 6–12 months of rental income history before approving a cash-out refinance. That window exists so lenders can verify the property generates real income at a stable rate.

Here is the typical sequence for navigating lender requirements:

- Purchase and rehab. Use cash, a hard money loan, or a private lender to fund acquisition and renovation.

- Place a qualified tenant. Document the lease, collect rent, and build a payment history.

- Wait out the seasoning period. Most conventional lenders require 6 months minimum; some require 12.

- Order an appraisal. The appraised ARV determines your refinance loan amount at 75% LTV.

- Close the cash-out refinance. Recover your invested capital and prepare it for the next acquisition.

- Repeat. The recovered cash becomes the down payment and rehab fund for the next property.

DSCR loans have become the standard refinance tool for BRRRR investors because they qualify based on the property's rental income rather than the investor's personal debt-to-income ratio. This matters enormously for scaling. Once you own three or four properties, your personal DTI can disqualify you from conventional financing even if every property cash flows well. DSCR loans sidestep that bottleneck entirely.

Two common mistakes at this stage: refinancing too early before seasoning is complete, which lenders will reject outright, and overleveraging by pulling out every possible dollar regardless of the resulting debt service. A refinance that returns cash is useless if the new monthly mortgage payment exceeds your net rental income.

What are the biggest risks in the BRRRR method?

The BRRRR method rewards discipline and punishes guesswork. The most common failure points are predictable, and most of them involve overestimating numbers at the start of a deal.

- Overestimating ARV. Inflated after-repair values lead to a refinance that returns less cash than expected, or no cash at all. Overestimating ARV creates cash flow shortfalls even when the refinance technically closes.

- Underestimating rehab costs. Skipping the contingency budget is the fastest way to run out of money mid-renovation. Structural surprises are not rare. They are routine in distressed properties.

- Ignoring seasoning requirements. Investors who plan to refinance immediately after renovation hit a wall. The holding cost gap between rehab completion and refinance approval is the most common BRRRR failure point.

- Emotional overbidding. Paying retail price for a property because you love the neighborhood destroys the 70% rule math before the deal even starts.

- Forcing BRRRR on bad deals. Successful investors source off-market and distressed properties that meet strict purchase criteria. Applying BRRRR to a retail-priced listing rarely works.

"The math either works before you buy, or it never will. No amount of renovation skill fixes an overpaid acquisition."

A concrete example: an investor buys a property at $120,000 with an estimated ARV of $160,000 and $20,000 in planned repairs. The 70% rule says the maximum offer is ($160,000 × 0.70) minus $20,000, which equals $92,000. Paying $120,000 means the investor is already $28,000 over the safe threshold before a single nail is driven. The refinance will not return enough capital to repeat the cycle.

Key Takeaways

The BRRRR method works because it recycles one capital pool across multiple properties, building rental portfolios faster and more efficiently than traditional buy-and-hold investing.

| Point | Details |

|---|---|

| 70% rule is non-negotiable | Calculate (ARV × 0.70) minus repair costs before making any offer. |

| Rehab for appraisal, not aesthetics | Add bathrooms and fix major systems; skip luxury finishes that appraisers ignore. |

| Budget a 10–20% contingency | Hidden structural costs are routine in distressed properties and will appear. |

| DSCR loans unlock portfolio scaling | Qualifying on property income avoids personal DTI limits as your portfolio grows. |

| Seasoning gaps require cash reserves | Plan to cover 6–12 months of holding costs before refinance capital returns. |

BRRRR in 2026: what disciplined investors know

I have watched investors chase BRRRR deals in every kind of market, and the ones who consistently succeed share one trait: they treat it as a math problem, not a real estate fantasy. The method is not about getting rich on one clever flip. It is about building a repeatable system where each deal funds the next.

Higher interest rates in 2025 and 2026 have made the refinance step more expensive than it was three years ago. That does not kill the strategy. It raises the bar for deal quality. Good math and discipline override market conditions. Investors who relied on cheap debt to paper over weak deals are the ones struggling now.

BRRRR is also not a passive strategy. During rehab, you are a project manager. During tenant placement, you are a landlord. Investors who treat it like a set-and-forget system consistently underperform. The ones who stay close to their numbers, their contractors, and their tenants build portfolios that actually cash flow.

My honest advice: start with one deal, run the numbers conservatively, and do not touch the refinance until the seasoning period is fully satisfied. Slow, correct cycles beat fast, broken ones every time.

— ARX

Deal-zilla tools for your next BRRRR cycle

Running BRRRR successfully means knowing your numbers before you make an offer, not after.

Deal-zilla gives real estate investors the analytical tools to evaluate ARV, model rehab costs, and project rental income before committing to a deal. The platform's BRRRR calculator and deal analyzer let you stress-test every cycle, from purchase price through refinance, so you know exactly where your capital goes and when it comes back. Serious investors use Deal-zilla to track deal performance, compare rental projections, and avoid the overestimation mistakes that sink most BRRRR attempts. Run your next deal through Deal-zilla before you sign anything.

FAQ

What does BRRRR stand for in real estate?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It is a real estate investment strategy designed to recycle capital across multiple rental property acquisitions.

How does the 70% rule apply to BRRRR?

The 70% rule sets your maximum purchase price at (ARV × 0.70) minus estimated repair costs. Staying at or below this threshold creates enough equity to support a 75% LTV cash-out refinance.

How long does the BRRRR seasoning period take?

Most lenders require 6–12 months of documented rental income before approving a cash-out refinance. Investors must cover holding costs during this period using cash reserves.

What is a DSCR loan and why do BRRRR investors use it?

A DSCR loan qualifies based on the property's rental income rather than the investor's personal income or debt-to-income ratio. This makes it the preferred refinance tool for investors scaling beyond three or four properties.

Can BRRRR still work in 2026 with higher interest rates?

Yes. Higher rates reduce margins but do not eliminate the strategy. Investors who source off-market deals and apply strict purchase criteria still execute profitable BRRRR cycles in the current market.